The Reserve Bank of India (RBI) released its Draft Guidance on Regulatory Expectations for Data Governance on 15 July 2026, inviting public comments. The draft introduces several important concepts in enterprise data governance, many of which have already been incorporated into the DGPSI (Data Governance and Protection Standard of India) framework. One of the most significant among them is the concept of Single Source of Truth (SSOT) in data architecture.

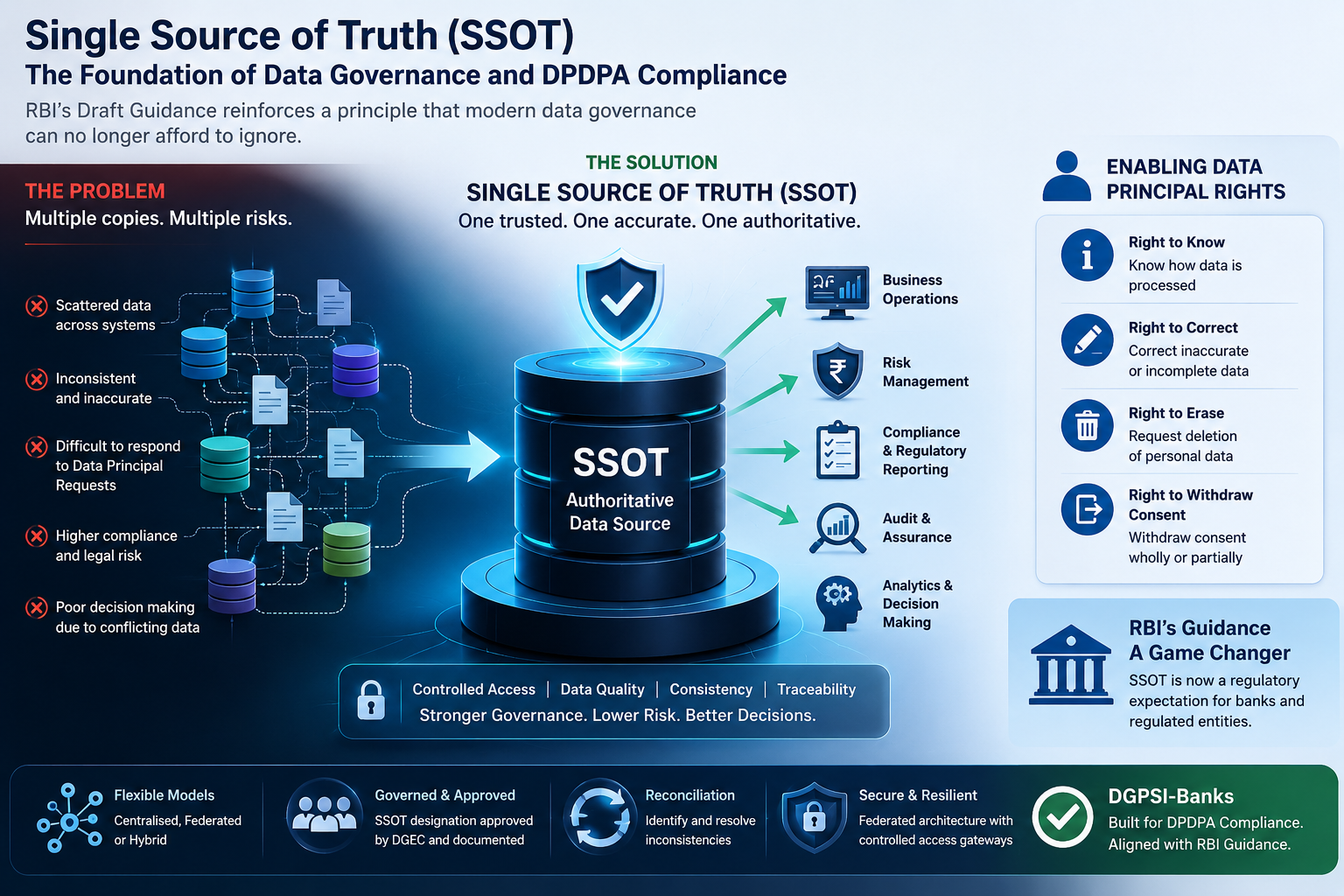

While designing a DPDPA-compliant Data Governance and Protection Management System (DGPMS), one of the most challenging areas is the implementation of the Data Principal Rights Management System. A Data Principal may exercise several statutory rights, including the right to know how personal data is being processed, the right to correct information, the right to erase data, or the right to withdraw consent either wholly or partially.

Effective implementation of these rights requires a well-designed data governance architecture. If multiple, uncontrolled copies of personal data are scattered across different systems, applications, or business units, responding accurately to such requests becomes difficult, expensive, and sometimes impossible. Unless the organisation has complete visibility over every instance of the data, compliance with DPDPA obligations cannot be assured.

In contrast, when every data element has a clearly identified authoritative version, the data remains accurate, current, and manageable. Corrections, deletions, consent withdrawals, valuation, and audit trails can all be executed with confidence and consistency.

For decades, information security professionals have advocated distributed storage architectures to minimise the risk of a single point of failure. Concentrating all data in one repository was traditionally viewed as increasing cyber risk by creating an attractive target for attackers.

However, the legal obligations arising under modern privacy and data protection laws have altered this perspective. Today, the absence of a clearly defined authoritative data source can itself become a significant compliance risk. Organisations are increasingly expected to demonstrate that they know exactly where personal data resides and can act upon it without ambiguity.

From a governance perspective as well, different business functions—operations, risk management, compliance, audit, and senior management—must make decisions based on the same trusted data. Competing versions of the same data inevitably lead to inconsistent reporting, flawed analytics, and poor decision-making.

The challenge, therefore, is no longer merely securing data. It is about balancing cybersecurity requirements with governance and regulatory obligations.

The RBI’s explicit adoption of the Single Source of Truth (SSOT) principle is therefore a landmark development. It will require many banks and other regulated entities to revisit and significantly redesign their existing data architecture and governance practices.

The draft guidance requires that:

- Every Regulated Entity (RE) should establish and maintain a Single Source of Truth (SSOT) for every data element.

- No parallel or competing authoritative sources should exist for the same data element.

- All downstream systems, analytical models, reports, and business processes should derive their data from the designated SSOT.

Importantly, the RBI does not prescribe a single implementation model. A Regulated Entity may adopt a centralised, federated, or hybrid architecture, provided the SSOT framework ensures:

- clear identification of the authoritative source for every data element;

- consistency of data across business, risk, compliance, and all other organisational functions; and

- complete traceability of aggregated data and reports.

The draft further requires that:

- the designation of the SSOT, and any subsequent changes, must be approved by the Data Governance Executive Committee (DGEC) and documented; and

- the Data Governance Committee (DGC) should be informed of such decisions.

In addition, every Regulated Entity should establish robust reconciliation mechanisms to identify and resolve inconsistencies between the SSOT and downstream data repositories.

The RBI has also recognised that the risks associated with centralisation can be mitigated through federated or hybrid architectures, where data may remain physically distributed while being governed through a well-defined authoritative source and controlled access mechanisms. Such architectures can provide the benefits of SSOT without compromising resilience or security.

This is likely to become one of the most significant implementation challenges for banks and other RBI-regulated entities over the coming years.

The DGPSI-Banks framework already incorporates these governance principles within its DPDPA compliance methodology. The RBI’s draft guidance further validates this approach and provides an additional regulatory impetus for organisations to strengthen their data governance architecture around the concept of a trusted and authoritative Single Source of Truth.

Watch out for the Naavi’s “Gateway Risk Management System” to elaborate how the balancing can be achieved between the SSOT principle and mitigation of the Single Source of Failure risk. (SSOF).

Naavi

On August 21, 22 and 23, FDPPI will be conducting the first CIDA (Certified Independent Data Auditor) program in Bangalore.

On August 21, 22 and 23, FDPPI will be conducting the first CIDA (Certified Independent Data Auditor) program in Bangalore.

")